At such levels, finding value, particularly in large-cap stocks, becomes more challenging.

However, here are three stocks that continue to be undervalued despite the significant market surge. These stocks have been selected using data from the Equitymaster Stock Screener.

To identify undervalued options, specific criteria were applied, including a price-to-earnings ratio below 10, a price-to-book value under 1, and a consistent history of profitability and dividend payouts.

Please note, this editorial is for informational purposes only and not intended as stock investment advice.

It’s important to keep in mind that valuation is a subjective concept; what one investor believes to be undervalued may not be the same for another.

This means that while valuation analysis offers insights, it is not a precise or absolute science; rather, it functions best when used as a guiding framework in conjunction with the knowledge of its limitations and complementary techniques.

Oil and Natural Gas Corporation (ONGC)

ONGC is a Maharatna company. It is India’s largest crude oil and natural gas producer, contributing around 71% to Indian domestic production.

Crude oil is the raw material used by downstream companies like IOC, BPCL, HPCL, and MRPL (last two are subsidiaries of ONGC) to produce petroleum products like petrol, diesel, kerosene, naphtha, and cooking gas LPG.

The stock currently trades at a price-to-earnings (PE) of seven times and a price to book (PB) of 0.8 times, according to the Equitymaster screener. The company has a consistent track record of dividend payments, with a dividend yield of over 5%.

On the financial front, the company reported revenues of ₹1,57,911.1 crore for Q2FY26 against ₹1,59,331.1 crore year-on-year. ONGC reported a net profit of ₹12,275.0 crore for Q2FY26 against ₹9,853.6 crore year-on-year. The increase in net profits can mainly be attributed to its subsidiaries, HPCL and MRPL.

For FY26, ONGC management is expecting oil production to reach 20 million metric tonnes. As far as gas is concerned, the management expects it to be slightly lower than the 21.5 BCM that was projected.

Moving ahead, ONGC has in the past faced issues with declining and mature fields. However, with BP-led TSP advancing for redevelopment of the MH Field, the scheme for revival of KG-98/2, and the combined Western Offshore Development Plan, ONGC is positioned to counterbalance declines from mature fields.

The accelerated monetization of new hydrocarbon discovery, alongside a sharper focus on deepwater and ultra-deepwater exploration is expanding ONGC’s resource base.

According to the management, these efforts, accompanied by enterprise-wide cost optimization and digital integration work across workflows, are expected to boost operational efficiency and reinforce ONGC’s resilience in the quarters ahead.

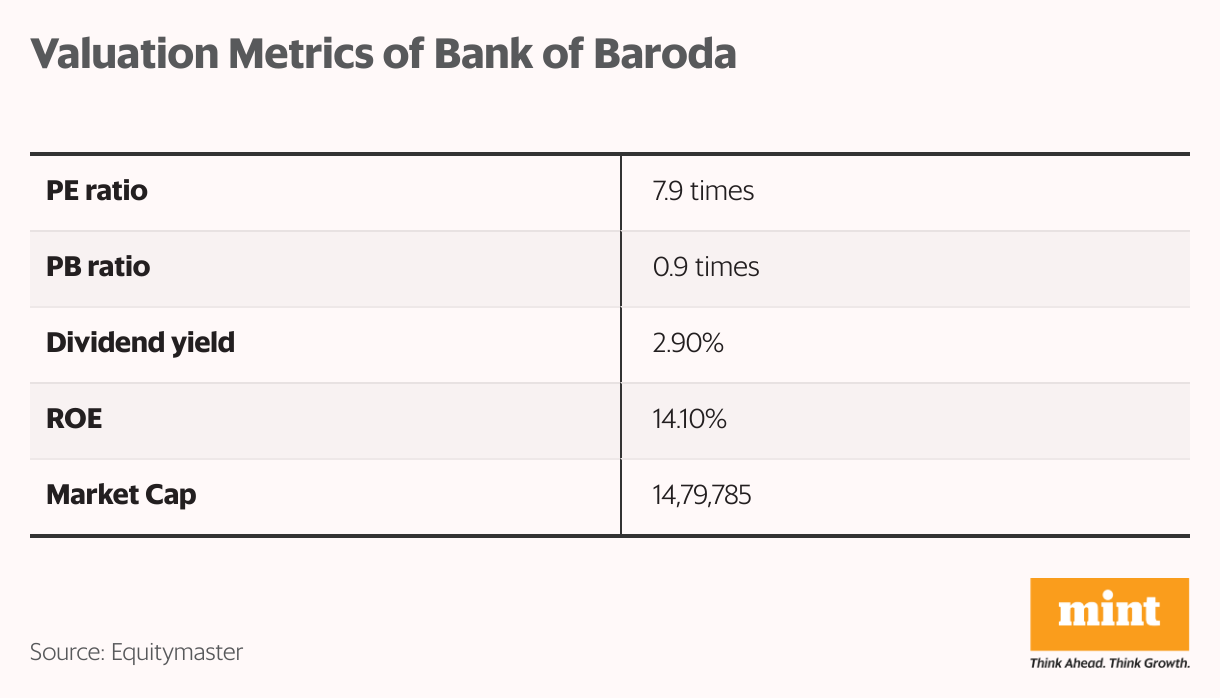

Bank of Baroda

The bank is the second-largest PSU bank in terms of market capitalization.

Bank of Baroda provides personal, business, corporate, international, treasury, and rural banking services, including deposits, loans, and insurance. It operates in 17 countries with 84 overseas branches.

In 2019, it merged with Dena Bank and Vijaya Bank, boosting its network to over 9,500 branches, 13,400 ATMs, and service to 120 million customers.

The stock currently trades at a PE of 7.9 times and a price -to-book value of 0.9 times. The bank has a consistent track record of dividend payments, with a dividend yield of nearly 2.9%.

On the financial front, the bank reported a good set of numbers for Q2FY26. Net interest income improved to ₹13,126.9 crore from ₹12,636.0 crore year-on-year. Net profits saw a decline to ₹5,070.3 crore from ₹5,455.0 crore year-on-year.

It’s pertinent to note that Q2FY26 results must be read in the context that in Q2 of FY25 the bank had a one-off recovery from written-off accounts, which elevated the base.

Without the one-off item of last year, the profit has grown by 22%.

Moving ahead, the management has given a guidance on advances of 11-13% growth for this year in a recent analyst meet. The retail growth in advances is expected to be strong and would continue following a trend of 18-20% for last many quarters.

In terms of net interest margins, the management is expecting the same would be somewhere between 2.85%-3%.

Overall, Bank of Baroda is likely to see improvements driven by steady profit growth, improving asset quality, and strong capital adequacy.

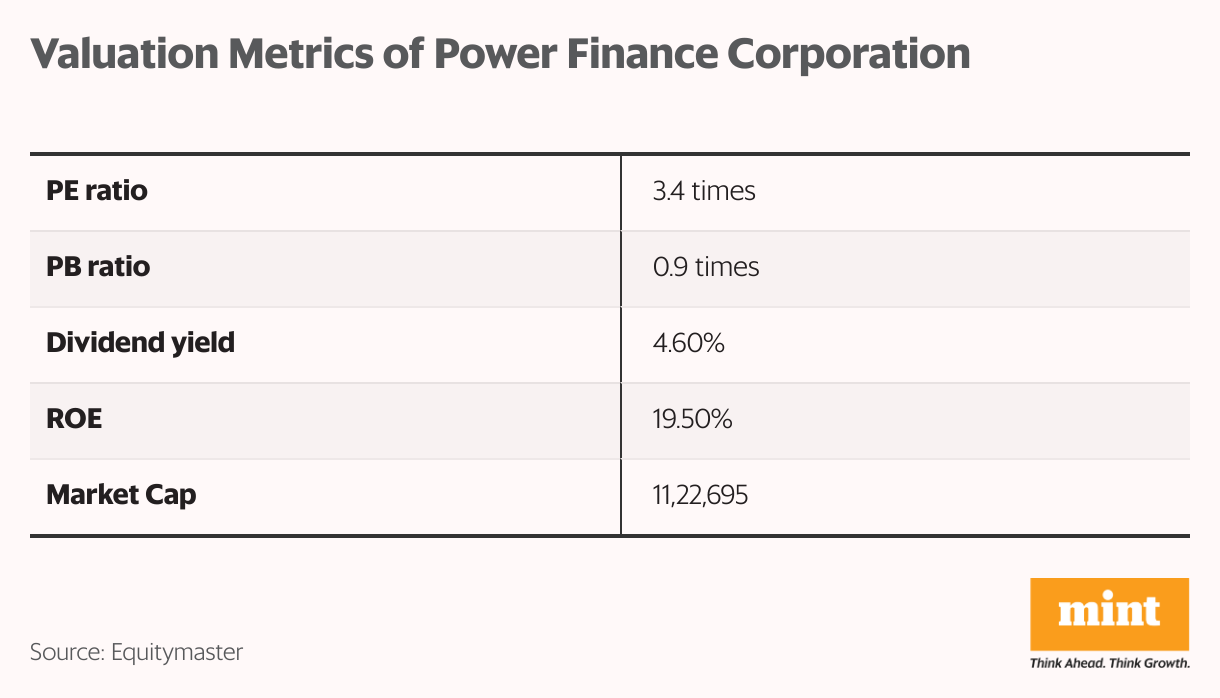

Power Finance Corporation

Power Finance Corporation (PFC) is a leading Maharatna public sector NBFC under India’s Ministry of Power, specialising in financing power generation, transmission, distribution, and related infrastructure projects.

The stock currently trades at a PE of just 3.4 times and a PB of 0.9 times. The company has a consistent track record of dividend payments, with a dividend yield of nearly 4.6%.

On the financial front, PFC saw interest earned rise to ₹28,890.2 crore for Q2FY26 against ₹25,721.8 year-on-year. The net profits during Q2FY26 were 7,834.4 crore vs ₹7,214.9 crore year-on-year.

Moving ahead, Power Finance Corporation benefits from strong positioning in India’s expanding power sector, particularly renewables.

The company has a strong loan book, driven by renewable financing growth. The asset quality of the company is good.

Conclusion

Investing in stocks that seem undervalued requires careful consideration.

Such stocks may be undervalued or oversold, presenting potential buying opportunities, especially if the low price is due to temporary factors.

However, caution is needed, even if some stocks may have value. Investors need to do thorough research into the reasons for the undervaluation.

Investors should evaluate the company’s fundamentals, corporate governance, and valuations of the stock as key factors when conducting due diligence before making investment decisions.

Happy Investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com.